Brazil is exceptional with its beautiful beaches, vast lush land mass and optimism (sounds like the US). I am currently in the center of the scaled biofuels world and it literally smells sweet - at least for Brazil. That sweet smell is alcohol in the air. The alcohol (ethanol) is being derived from sugar cane which rich rainforest cleared land and climate permits. Ethanol produced from sugar cane is used as a fuel for vehicles here on a scale no other country has ever been capable. No other country can replicate Brazil's unique cleared rainforest climate and soils.

Brazil has also recently discovered a lot of relatively high cost conventional hydrocarbons a ways offshore - although this oil is at least five to ten years away from production.

Brazil is an exception in so many way that one wonders if it should be used as an example. I will be posting some observations over the next few days. The first is how well the economy appears to be doing here. Factories are producing, office workers are optimistic, restaurants and stores are busy, the woes of debt laden developed nations and consumers are far from consideration. Demand is good for everything Brazilian.

Monday, September 28, 2009

Thursday, September 24, 2009

Financial Times and Floating Storage

I was quoted in a Financial Times story today on floating storage barrels coming ashore being an oil price lid for the moment:

“The contango has come down,” said Morgan Downey.....“There’s no incentive to keep it offshore any more.” (Financial Times)

Increasing Diversity of Transportation Fuels

As you will know from Oil 101, natural gas has been finding an increased use as an alternative to oil as a transportation fuel in a particular niche: natural gas is particularly suited to urban bus and trucking fleets as vehicles can be refuelled at the same spot each day and the distances vehicles can travel on a single refuelling is slightly more limited than with diesel.

Until relatively recently compressed natural gas (CNG) had been used mostly for buses and other urban people carriers. Now that natural gas fundamentals have changed such that natural gas prices are extremely low relative to oil, it makes not just environmental sense, but has also become economically sound for private businesses to convert.

An interesting and well researched story today by Brian Baskin at Dow Jones describes how most beer in New York City is being, or will shortly be, delivered with natural gas powered trucks rather than diesel.

Until relatively recently compressed natural gas (CNG) had been used mostly for buses and other urban people carriers. Now that natural gas fundamentals have changed such that natural gas prices are extremely low relative to oil, it makes not just environmental sense, but has also become economically sound for private businesses to convert.

An interesting and well researched story today by Brian Baskin at Dow Jones describes how most beer in New York City is being, or will shortly be, delivered with natural gas powered trucks rather than diesel.

Wednesday, September 23, 2009

Ahoy Ahoy: Floating Storage Coming Ashore

Chart 1 shows total US oil inventories by week. Total US oil inventories increased by 8.5 million barrels. The second chart (Chart 2 below) shows US oil demand which looked as if it may have reached an inflection point over the past month (US gasoline demand is strong, offsetting weak diesel and jet demand).

One thought is that the increase in inventories could be oil in floating tankers coming onshore now that the forward curve is flattening which removes the incentive to store. So either the forward curve goes into steep contango again or flat price oil is about to fall (or a combination of both) as this floating material comes onshore. Or perhaps extrapolating a single week’s counter trend data point (the trend being falling inventories and higher prices) is not such a wise decision?

The last few weeks of September are always quite a volatile time for US demand and inventories. We are in the low demand shoulder period between driving and heating oil seasons. This week's numbers could be reflecting the data noise during this seasonal transition.

Oil Discoveries Up...Still Not Enough

Although new oilfields are discovered every year, it is unfortunately a fact that the number of large oilfield discoveries has been in a multi-decades long decline (see Oil 101 for a fuller description of discoveries and reserves).

The few larger discoveries over the past ten years with potentially economically recoverable oil of 3 to 10 billion barrels (Gb) have been warmly greeted, but are insufficient in the grander picture.

To put everything in perspective with these large numbers, bear in mind that there are around 30 Gb of oil consumed each year worldwide and this number grows by 1-2% per year. So, in order to stand still, oil companies around the world have to discover at least 30 Gb of oil each year.

Discoveries of approximately 3-5 Gb of potentially economically recoverable oil off the US Gulf Coast in 2008, 5-10 Gb off Brazil in 2006, 9 Gb in the Caspian Sea off Kazakhstan in 2000, and 6-8 Gb in Iran in 1999 and 2003 were among the largest over the past ten years. There were of course other smaller discoveries in addition to revisions to the sizes of fields previously discovered.

Two newspapers are giving somewhat different perspectives on the long term decline in discovery rates.

The New York Times today states that despite insufficient new oilfield discoveries, one oil industry consulting group believes that higher prices are making up the difference by allowing for reserve expansion in oilfields which are already in production:

The few larger discoveries over the past ten years with potentially economically recoverable oil of 3 to 10 billion barrels (Gb) have been warmly greeted, but are insufficient in the grander picture.

To put everything in perspective with these large numbers, bear in mind that there are around 30 Gb of oil consumed each year worldwide and this number grows by 1-2% per year. So, in order to stand still, oil companies around the world have to discover at least 30 Gb of oil each year.

Discoveries of approximately 3-5 Gb of potentially economically recoverable oil off the US Gulf Coast in 2008, 5-10 Gb off Brazil in 2006, 9 Gb in the Caspian Sea off Kazakhstan in 2000, and 6-8 Gb in Iran in 1999 and 2003 were among the largest over the past ten years. There were of course other smaller discoveries in addition to revisions to the sizes of fields previously discovered.

Two newspapers are giving somewhat different perspectives on the long term decline in discovery rates.

The New York Times today states that despite insufficient new oilfield discoveries, one oil industry consulting group believes that higher prices are making up the difference by allowing for reserve expansion in oilfields which are already in production:

"New oil discoveries have totaled about 10 billion barrels in the first half of the year, according to IHS Cambridge Energy Research Associates. If discoveries continue at that pace through year-end, they are likely to reach the highest level since 2000....oil companies have found more oil than they produced for the last two years through a combination of exploration and field expansions." (NYTimes)Meanwhile, the Financial Times (FT table of some major recent discoveries here) states that while the ability to workover fields as a result of higher oil prices has improved recovery rates, it doesn't change the growing deficit between the lack of discoveries and demand:

"Game-changers locally, the finds do not alter things globally. They are much smaller than the supergiants of the last century, still producing at dwindling rates today ....while the industry is getting better at finding and producing oil – seismic surveys are more accurate and recovery rates higher – these are often incremental improvements rather than technological leaps. The world is still heading for an oil crunch.." (Financial Times)

Tuesday, September 22, 2009

CNBC Commodities

On CNBC's Closing Bell live today I spoke with Maria Bartiromo about commodities.

(click here to view on CNBC's site if it doesn't open below)

(click here to view on CNBC's site if it doesn't open below)

Monday, September 21, 2009

Raising Retail Taxes on Oil is a Bad Idea

An article by Thomas Friedman in the NY Times today calls for the US government to raise retail taxes on oil. In the past I have discussed why imposing European oil tax regimes in the US is not appropriate.

Even if such a tax could be imposed in the US, Mr. Friedman suggests paying down deficits and funding other non-transportation goals. This would be a bad idea. To avoid negative externalities to the economy, any money raised should be spent improving mass transit, freight rail, and shipping. Otherwise it would be a hugely negative tax on trade and commerce.

There needs to be a US solution which meets the particular challenges of US transportation patterns. and which is politically tenable. Such a a politically acceptable solution could be a Vehicle Efficiency Market.

Even if such a tax could be imposed in the US, Mr. Friedman suggests paying down deficits and funding other non-transportation goals. This would be a bad idea. To avoid negative externalities to the economy, any money raised should be spent improving mass transit, freight rail, and shipping. Otherwise it would be a hugely negative tax on trade and commerce.

There needs to be a US solution which meets the particular challenges of US transportation patterns. and which is politically tenable. Such a a politically acceptable solution could be a Vehicle Efficiency Market.

Sunday, September 20, 2009

Oil and the White Swan Non-Event

The expected continues not to happen.

Black swan events tend to be thought of as low probability events which occur. There can also of course be events which are highly expected (White Swans ?) but which do not occur.

As a result of the 2005 hurricane season, 166 million barrels cumulatively were shut in. That was an extreme year for tropical storms. The 2009 hurricane season is now looking as if it will be the other extreme with no oil and gas production shut ins so far.

The US EIA carried out an analysis earlier this year and assigned a 4% probability to the 2009 hurricane season resulting in no shut ins. The EIA forecast a total cumulative shut in value of 4.5 million barrels of crude to be shut in. So far there has been no US Gulf Coast shut ins. The following chart of Google searches for the word hurricane (updated to Sep 13, 2009) nicely reflects the benign nature of the 2009 hurricane season to date.

Wednesday, September 16, 2009

Chinese Oil Demand Shock

Running through many historical scenarios for other developing nations such as Brazil and Thailand I have come to the stark conclusion that the market could be underestimating Chinese oil demand growth by a huge amount over the next 2 to 4 years.

China is at a major inflection point in terms of oil demand. This has been borne out by many other countries at similar development stages. If anything, China is 2-3 years overdue an oil demand growth spurt given its income growth. The August 2009 82% year/year jump in annual Chinese auto sales is a harbinger of what is about to come. That 82% is not a typo. China has skipped its traditional seasonal summer decline in vehicle sale entirely so far in 2009 (see chart below).

If China follows a similar pattern to other developing nations then Chinese demand is likely to not just grow by its past 5 year rate of around 5% per year over the next 2 years. Chinese oil demand is on the precipice of a significant jump in annual growth over the next few years. The absolute barrel volumes of oil are enormous.

China is at a major inflection point in terms of oil demand. This has been borne out by many other countries at similar development stages. If anything, China is 2-3 years overdue an oil demand growth spurt given its income growth. The August 2009 82% year/year jump in annual Chinese auto sales is a harbinger of what is about to come. That 82% is not a typo. China has skipped its traditional seasonal summer decline in vehicle sale entirely so far in 2009 (see chart below).

Chart: Chinese Total Monthly Vehicle Sales in Millions

(click to enlarge)

If China follows a similar pattern to other developing nations then Chinese demand is likely to not just grow by its past 5 year rate of around 5% per year over the next 2 years. Chinese oil demand is on the precipice of a significant jump in annual growth over the next few years. The absolute barrel volumes of oil are enormous.

Monday, September 14, 2009

What is it about 4.6 barrels per year?

Cats are curious

(a friend of mine behind the computer screen)

(a friend of mine behind the computer screen)

Since 1982 the number of people in the world has grown by almost 45% or 2 billion people (chart 1).

Oil supply has been unable to outpace population growth since the 1970s and has from 1982 until recently just been able to keep pace with demand (chart 2). What can one person do with 4.6 barrels (193 US gallons) per year? With a vehicle getting 30 miles per gallon one can drive an average of around 16 miles per day.

Why has per capita consumption been so stable since 1982 having grown at an increasing pace for the prior 120 years (chart 2 again)? The answer is that a new method of rationing demand emerged in 1983: benchmark pricing linked to transparent free liquid markets (see chapter 1 of Oil 101). Free markets and necessarily volatile oil price became the adjusting factor matching available supply to demand.

To put the global average of 4.6 barrels of oil consumption per year in perspective, the number of barrels consumed per person in 2008 in India was 0.9, China 2.2, Brazil 4.6, Germany 11.1 and the US 23.3.

Build your own chart of consumption patterns over time by clicking here (click the 'Play' button to start and the individual country to track over time - set X axis to 'Time' and Y axis to 'Oil Barrels Consumed per Person').

Tuesday, September 8, 2009

The End of Decline: Oil Demand Recovering

Ahead of OPEC members meeting Wednesday September 9 in Vienna, it is worth taking stock of why OPEC has no choice but to refrain from making any production changes and why they may in fact need a temporary tightening of compliance with existing quotas by up to 500,000 barrels per day in order to maintain prices above the low US$70s per barrel. Compliance with the 4.2 million barrels per day (Mb/d) cuts announced by OPEC members in late 2008 is currently around 3Mb/d.

--------------

During the 2008-2009 recession global oil demand fell by 2 Mb/d from 86 to 84Mb/d (chart 1). Global demand appears to have stabilized and is beginning to grow again. The charts in this post (click to enlarge) use monthly data and 12 month rolling averages to adjust for seasonality.

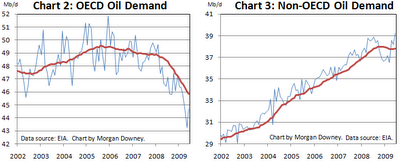

Almost all the global decline was concentrated in developed OECD nations (chart 2). Less developed non-OECD nations such as China and India only saw a temporary stagnation and are now exhibiting growing demand again (chart 3).

Almost all the global decline was concentrated in developed OECD nations (chart 2). Less developed non-OECD nations such as China and India only saw a temporary stagnation and are now exhibiting growing demand again (chart 3).

Of the OECD decline, one third came from the US, one third from OECD Europe, and one third came from the remaining developed OECD countries.

Of the OECD decline, one third came from the US, one third from OECD Europe, and one third came from the remaining developed OECD countries.

The US accounts for just under 23% and Europe 18% of 2009 global oil demand. Oil demand in the US and Europe has yet to stop falling (see charts 4 and 5).

Oil demand in the US was destroyed more in absolute barrels over the past few years than in any other region.

Oil demand in the US was destroyed more in absolute barrels over the past few years than in any other region.

The severe demand destruction in the US had a lot to do with current US oil consumption patterns (76% of Americans get to and from work by driving alone) and infrastructure (average US vehicle fleet efficiency is less than half that of available technology). Relatively inefficient consumption allows for swift efficiency gains compared with other parts of the world which are already at or close to maximum technically available oil consumption efficiency.

Looking at total US oil demand (chart 4) one may perceive that it is in a steady decline which can perhaps be extrapolated into the future. However, delving deeper into the data provides clues as to exactly why US demand is declining and why we may be at or quickly approaching the end of the decline in total US demand.

The total number of miles driven on US highways has stabilized and is increasing (chart 6).

This stabilization and increase in highway miles driven is showing up in US gasoline demand which is no longer falling and has begun to grow again (chart 7). Gasoline demand accounts for almost half US oil consumption.

This stabilization and increase in highway miles driven is showing up in US gasoline demand which is no longer falling and has begun to grow again (chart 7). Gasoline demand accounts for almost half US oil consumption.

The recovery in gasoline demand is because people are cutting back on vacation spending by driving rather than flying to holiday spots. This certainly syncs with the fall in jet fuel consumption (chart 8) and anecdotal evidence. Businesses have also been cutting back on flights.

The recovery in gasoline demand is because people are cutting back on vacation spending by driving rather than flying to holiday spots. This certainly syncs with the fall in jet fuel consumption (chart 8) and anecdotal evidence. Businesses have also been cutting back on flights.

The decline in jet fuel consumption is more than offset by the increase in gasoline consumption. Combined, jet fuel and gasoline demand (together 57% of total US oil demand) are beginning to recover (chart 9).

The decline in jet fuel consumption is more than offset by the increase in gasoline consumption. Combined, jet fuel and gasoline demand (together 57% of total US oil demand) are beginning to recover (chart 9).

Where is the remaining weakness in US oil demand? It is in industrial oil demand. Demand for distillate (diesel and heating oil), residual fuel oil (mostly used for shipping and a little for electrical power generation) and other oils (lubes, waxes, asphalt, plastics and a bunch of other oils).

Where is the remaining weakness in US oil demand? It is in industrial oil demand. Demand for distillate (diesel and heating oil), residual fuel oil (mostly used for shipping and a little for electrical power generation) and other oils (lubes, waxes, asphalt, plastics and a bunch of other oils).

Aggregating these three categories of US oil demand into “Industrial” demand, these industrial oils account for 43% of total US oil demand (chart 11).

Aggregating these three categories of US oil demand into “Industrial” demand, these industrial oils account for 43% of total US oil demand (chart 11).

To see a recovery in US industrial oil demand there would have to be a recovery in consumer spending (linked to unemployment, housing and the savings rate), manufacturing activity (especially autos), and private services sector activity. Most indicators in these macroeconomic areas have begun to stabilize and even improve over the past couple of months.

Conclusion: US industrial oil demand is currently the weakest part of global oil demand and the largest component of global oil demand yet to cease declining. Non-oil macroeconomic indicators suggest that an end to the decline in US industrial oil demand is imminent.

Despite the weakness in OECD oil demand and US industrial oil demand in particular, global oil demand has stabilized and begun growing due to non-OECD demand.

So why have oil prices stabilized in the US$65-75 per barrel range if the reduction in demand has been plumbed at 2Mb/d and the fall is over?

At the end of 2008 OPEC members removed close to 3Mb/d from supply. This was the amount required to stabilize and reduce OECD land based storage. OECD land based storage is the easiest storage to track.

The problem with focusing on OECD land based storage which is no longer increasing is that it ignores difficult to measure global floating storage and non-OECD land based tanks. Floating storage (see chart below) and non-OECD storage continue to creep higher. There needs to be an elimination of inventory growth in these difficult to measure areas in order to hold the prices gains witnessed in 2009.

This elimination of inventory growth can come from the recovery of global demand which appears to be just beginning or a further reduction in supply from OPEC. The number required is around 0.5Mb/d.

At the OPEC meeting this coming Wednesday, September 9, OPEC members have no choice but to maintain existing production cuts. In fact, until nascent global demand growth strengthens, OPEC members may need a temporary 0.5Mb/day improvement in cut compliance (compliance with 4.2Mb/d cuts announced in late 2008 is only around 3Mb/day) in order to stall the increases in floating and non-OECD storage, bring the global market into balance (a balanced market has inventories neither increasing nor decreasing) and hold onto 2009 price gains.

--------------

During the 2008-2009 recession global oil demand fell by 2 Mb/d from 86 to 84Mb/d (chart 1). Global demand appears to have stabilized and is beginning to grow again. The charts in this post (click to enlarge) use monthly data and 12 month rolling averages to adjust for seasonality.

The US accounts for just under 23% and Europe 18% of 2009 global oil demand. Oil demand in the US and Europe has yet to stop falling (see charts 4 and 5).

The severe demand destruction in the US had a lot to do with current US oil consumption patterns (76% of Americans get to and from work by driving alone) and infrastructure (average US vehicle fleet efficiency is less than half that of available technology). Relatively inefficient consumption allows for swift efficiency gains compared with other parts of the world which are already at or close to maximum technically available oil consumption efficiency.

Looking at total US oil demand (chart 4) one may perceive that it is in a steady decline which can perhaps be extrapolated into the future. However, delving deeper into the data provides clues as to exactly why US demand is declining and why we may be at or quickly approaching the end of the decline in total US demand.

The total number of miles driven on US highways has stabilized and is increasing (chart 6).

To see a recovery in US industrial oil demand there would have to be a recovery in consumer spending (linked to unemployment, housing and the savings rate), manufacturing activity (especially autos), and private services sector activity. Most indicators in these macroeconomic areas have begun to stabilize and even improve over the past couple of months.

Conclusion: US industrial oil demand is currently the weakest part of global oil demand and the largest component of global oil demand yet to cease declining. Non-oil macroeconomic indicators suggest that an end to the decline in US industrial oil demand is imminent.

Despite the weakness in OECD oil demand and US industrial oil demand in particular, global oil demand has stabilized and begun growing due to non-OECD demand.

So why have oil prices stabilized in the US$65-75 per barrel range if the reduction in demand has been plumbed at 2Mb/d and the fall is over?

At the end of 2008 OPEC members removed close to 3Mb/d from supply. This was the amount required to stabilize and reduce OECD land based storage. OECD land based storage is the easiest storage to track.

The problem with focusing on OECD land based storage which is no longer increasing is that it ignores difficult to measure global floating storage and non-OECD land based tanks. Floating storage (see chart below) and non-OECD storage continue to creep higher. There needs to be an elimination of inventory growth in these difficult to measure areas in order to hold the prices gains witnessed in 2009.

This elimination of inventory growth can come from the recovery of global demand which appears to be just beginning or a further reduction in supply from OPEC. The number required is around 0.5Mb/d.

At the OPEC meeting this coming Wednesday, September 9, OPEC members have no choice but to maintain existing production cuts. In fact, until nascent global demand growth strengthens, OPEC members may need a temporary 0.5Mb/day improvement in cut compliance (compliance with 4.2Mb/d cuts announced in late 2008 is only around 3Mb/day) in order to stall the increases in floating and non-OECD storage, bring the global market into balance (a balanced market has inventories neither increasing nor decreasing) and hold onto 2009 price gains.

Tuesday, September 1, 2009

Low Volume Week

This is the last week of the Summer US driving season. With US bank holiday Labor Day coming up next monday and the UK end of August bank holiday on the Monday just gone, liquidity in oil markets is low. During such periods of low liquidity, oil market reaction to events tends to be a little larger than usual. I was quoted in the Wall Street Journal:

"On any day that you're going to have low liquidity and there's going to be a move in the market, that move is generally going to be exaggerated," said Morgan Downey (WSJ)

Scale of Replacing Fossil Fuels in Perspective

The physicist David MacKay has written an interesting piece on renewable energy completely replacing fossil fuels. The scale of the challenge is immense - but not insurmountable:

The repayment time horizon for wind, solar, geothermal, nuclear and other sources of power tends to be much longer than that of fossil fuels.

There are many financial solutions to this timing disadvantage. One solution being used is for the government to step in on behalf of taxpayers and quicken the pace which investors get their money back. Such government spending is unsustainable.

Wind and other renewables have to compete without subsidies if they are to be scaled to the size David MacKay mentions. A shift to renewables on a MacKay scale may have to wait until fossil fuels production declines. Only then will high energy prices provide a sufficiently quick pace for renewable investors.

"Today, the average European consumes 120 kilowatt-hours per day. That’s more than double the world average, but lifestyle changes and determined switches to more efficient technologies for transport and heating might enable a modern European quality of life to be enjoyed for an energy cost close to the current world average, perhaps 60 kilowatt-hours per day a person.This shift toward renewables on such a large scale will only take place if it there is an economic advantage in doing so. This will require a change in the time horizon energy investors seek. For example, most oil and gas investors look to have their initial investment repaid in under 12 years (see the PE ratios of top oil and gas producers).

What sort of building project is required to deliver that much energy?

For illustration, imagine getting one-third of that energy from wind, one-third from desert solar power and one-third from nuclear power.

If a country with the size and population of Britain — 61 million people — adopted that mix, the land area occupied by wind farms would be nearly 10 percent of the country, or roughly the size of Wales. The area occupied by desert solar power stations — in the case of Britain, they would have to be connected by long-distance power lines — would be five times the size of London. The 50 nuclear power stations required would occupy a more modest 50 square kilometers.

The effort required for a plan like that is very large, but imaginable. Countries that claim to be serious about creating an alternative energy future need to choose a plan, stop arguing and get building." (David MacKay/NYTimes)

The repayment time horizon for wind, solar, geothermal, nuclear and other sources of power tends to be much longer than that of fossil fuels.

There are many financial solutions to this timing disadvantage. One solution being used is for the government to step in on behalf of taxpayers and quicken the pace which investors get their money back. Such government spending is unsustainable.

Wind and other renewables have to compete without subsidies if they are to be scaled to the size David MacKay mentions. A shift to renewables on a MacKay scale may have to wait until fossil fuels production declines. Only then will high energy prices provide a sufficiently quick pace for renewable investors.